Shortly after my last article (Rau’s World – Public Sector Shakeup) (2 December 2016), Self Insurers of South Australia (“SISA”) published its Position Statement on the privatisation of public sector workers compensation. SISA stated, in part:

“We take the view that to do this at the expense of a very efficient and cost-effective public sector self-insurance system sacrifices the interests of the affected injured workers and the taxpayer, who will have to foot the bill for much increased costs…

SISA can’t see a single practical or financial thing that says that this is a good idea. We can see plenty of reasons why it isn’t. Yet it seems to be happening anyway….

If private underwriting and pocketing a large part of the employer-funded RTW fund is not the objective, the Government must say so. It must then explain why it is putting the interests of the taxpayer and current and future injured public sector workers at such risk by secretly disposing of a system that performs better than the system to which it is to be handed over.”

On 12 December 2016, Thompson Reuters Workers Compensation Report (“WCR”) (Issue 1094) published an article reporting on the SISA statement. WCR noted that:

“SA Industrial Relations Minister John Rau told WCR the proposed move was not a prelude to privately underwriting the State’s workers compensation Scheme. ‘Privatisation is not on the agenda’ he said…Rau’s spokesperson said the plan was about ‘centralising claims’ and he went on to assert that RTWSA’s premium management, funding and claims management/disputation ‘successes’ had made it a ‘good’ option for the new cohort of claims.”

So, Minister Rau has apparently ruled out private underwriting as a possible future for the workers compensation Scheme, but can we honestly believe this to be true?

The public rationalisation for the movement of the public sector claims into the registered Scheme does not stand up to scrutiny unless privatisation is the real rationale.

Let’s look at the rationale:

“Premium Management and Funding Successes”

These are largely smoke and mirrors. The funding turnaround was provided when Parliament handed the Corporation a new Act with capped benefits. The only part of the Scheme that did consistently well under the repealed legislation was the self-insured segment, including the public sector, from which the Government now seems intent on stripping self-insurance. In point of fact, the funding situation has actually gone backwards slightly since the RTW Act came into effect (ignoring the one off improvement conferred by the new Act between 2014-15 and 2015-16). In the latest annual report the underwriting result for the financial year ended 30 June 2016 is a negative $109,897.00 compared with a positive $1,344,602.00 for the previous year.

“Claim Management/Disputation Successes”

These are very hard to spot out here in the real world. If claims are accepted without proper scrutiny and investigation then of course dispute rates will fall but ultimately that will impact upon employers’ premium.

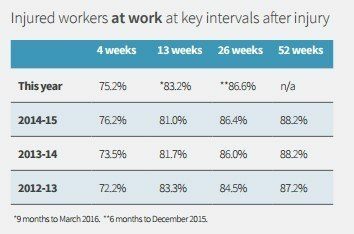

By and large the statistic of “injured workers at work at key intervals after injury” has remained fairly static from the 2012-13 year.[1]

Not much resounding success there and certainly nothing to suggest that this is a good option as claimed by the Minister.

“Centralising claims”

The aim of centralising claims management could equally be achieved administratively within the public sector by adopting a shared services model. Arguably there is no need for each public sector employer to have its own claims management team in diverse locations and so if the aim is to centralise claims management that could be more simply achieved administratively and without the loss of the key efficiency factor – self-insurance and the experienced and skilled workforce that currently exists.

The very fact that this obvious (and far less costly) approach appears to have been ignored clearly demonstrates that cash flow is not what this is about.

Let me make it quite clear. I am not opposed to privatisation of the Scheme.

The Scheme in Western Australia is largely privatised. There are nine insurers in addition to the statutory body and, admittedly from a distance, the Scheme appears to work quite well and the average premium rate is about 1.5% compared to the current rate of 1.95% in this State. Premium income in WA, however, is $1,023.6 million compared to $495 million in premium income in SA which is down from $645 million in the previous year.

The WA Scheme is attractive enough to involve nine insurers but, perhaps, the additional premium income which will be provided by the public sector is needed to make our Scheme similarly attractive.

If that is the case why isn’t the Government being honest and transparent about recognising this option and encouraging an open evaluation of the option?

I will also make it quite clear that I am very much in favour of promoting the advantages of self insurance (see my articles November 2011, 4 February 2016 and 3 December 2016) and I believe the planned surrender of public sector self insurance to be a retrograde step and one which will ultimately be financially disadvantageous for most of the Agencies.

So What is it all About Alfie?

The changes must be driven by the need to generate a great deal of new premium to make the Scheme attractive to insurers with privatisation being the ultimate goal. Privatisation will deliver the Government another massive windfall and another artificial budget surplus.

Consider this:-

“Writing third party insurance policies is not an essential service that should be delivered by Government. This initiative is anticipated to allow MAC to pay $500 million in surplus net assets to the Government by the end of 2016-17”

SA Treasurer Tom Koutsantonis, quoted in In Daily 17/7/14.

When Treasurer Tom Koutsantonis delivered the mid‑year Budget in December with a revised 2016-17 surplus expected to be $300 million he instanced a “better than expected” profit from the Motor Accident Commission in 2015-16 and cash from the Commission’s insurance set off saw an additional $327 million dividend paid into Government coffers this financial year.

In Daily reported on 12 December 2016 that:-

“After the MAC windfall, Koutsantonis was again forced to defend opening compulsory insurance provisions to private insurers, insisting that “no one can tell me or convince me that a monopoly Government institution can do it cheaper or better than the private sector” … “I expect there would be dramatic savings for consumers once we have a competitive market”, and going on to insist that the selloff would prove to be “the opposite of the ETSA privatisation”.

On 15 December 2016 the Australian reported that:-

“The race for the $750 million Australia wide portfolio being sold by South Australia’s Motor Accident Commission has emerged as one of the key contests for major office and industrial properties that will spill into the New Year … the MAC offer was billed as one of the largest offers in industrial property portfolios of the year and values have leapt since it was first mooted … Mr Koutsantonis has said the sale is a key component of the decision to move the provision of compulsory third party insurance to the private sector”.

Substitute RTWSA for MAC in the above quotations and try to explain why privatisation of the Scheme would not in fact be on the agenda!!

In delivering the immediate budget forecast Mr Koutsantonis was asked if it would be necessary to offer voters budget sweeteners in order to win next year’s election. Mr Koutsantonis said it would take “investing in things that are important to South Australians – investing in tax cuts, investing in priorities (such as) health, education, police …we’re not just here to make up the time until the 2018 election – we want to win”.

The spending on infrastructure and the like planned by the Government will likely shrink surpluses in future years … unless there is another major windfall!

This is all about the money but is it going to be short term gain for the Government but long term pain for injured public sector employees and higher overall cost to the majority of Crown agencies?

Could it also be about reducing public sector numbers and, therefore, further costs saving for the Government because there is the potential for about 150 claims jobs to be lost in the public sector?

The historical evidence is irrefutable. Self insurers as a cohort do it better and the public sector specifically outperforms the Scheme. With 18% of the Scheme by remuneration it had about 9.6% of the Scheme liability before the RTW Act came into effect. Self insurance status is a significant advantage that should not be surrendered lightly for short-term gain and electoral advantage. Any such decision deserves rigorous investigation and evaluation.

Don’t tell me it is all about “claims management/disputation successes or centralising claims management”. That is frankly rubbish and as SISA manager Robin Shaw succinctly puts it “SISA can’t see a single practical or financial thing that says this is a good idea. We can see plenty of reasons why it isn’t. Yet it seems to be happening anyway”.

One thing is for certain – it is all about the money!

RTWSA in Report 2015-16